Short-Term Rental Business Accounting: A Practical Guide to Clean Books

June 21, 2026

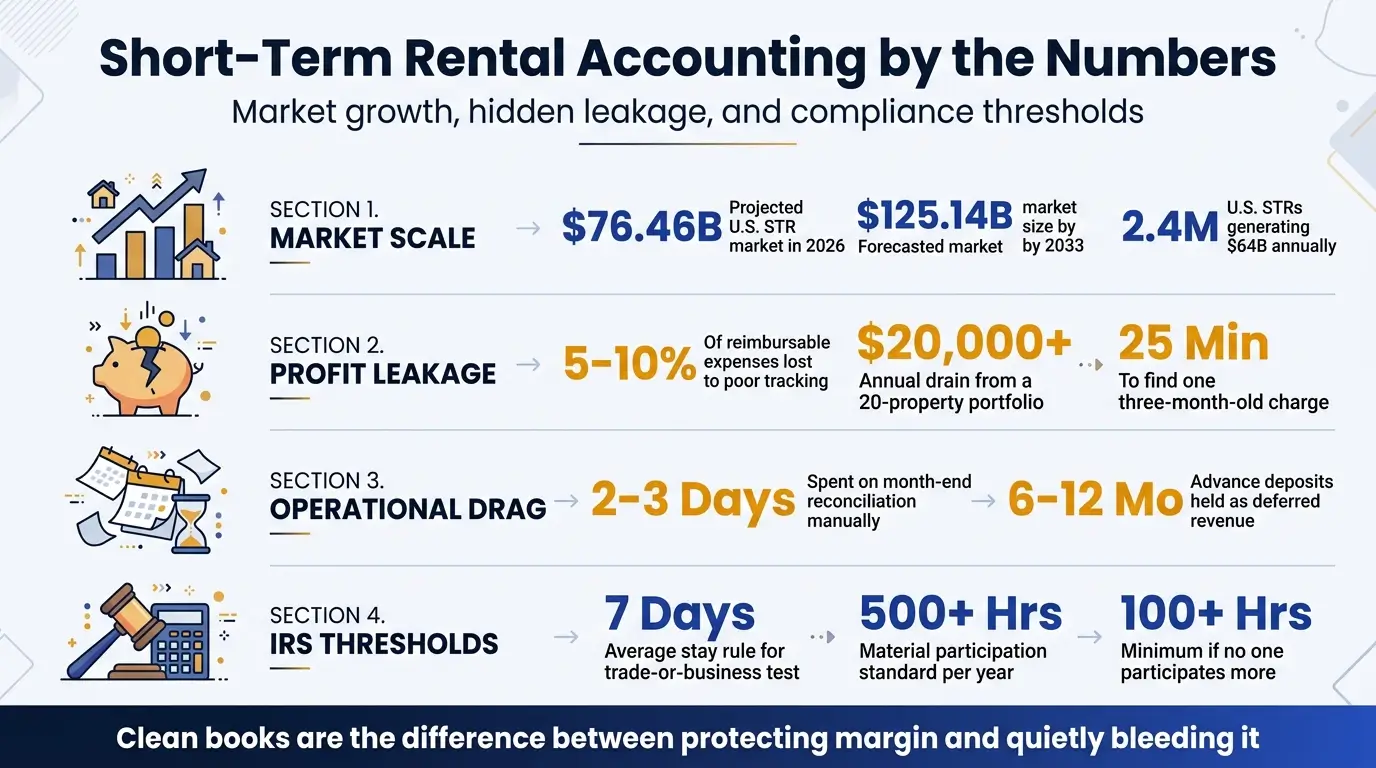

Property managers lose 5-10% of reimbursable expenses to poor tracking and reconciliation — a leak that can drain $20,000 or more annually from a 20-property portfolio.[3] If you run a short rental business, clean books aren't a back-office nicety. They're the difference between protecting margin and quietly bleeding it.

This guide is a practical operating manual for short-term rental (STR) accounting — not a generic bookkeeping primer. By the end, you'll have a repeatable system built on three pillars:

- Revenue classification and chart of accounts that mirror how STRs actually earn money

- Trust-account controls and monthly close that keep guest, owner, and operating funds separate

- Tax and compliance documentation aligned with the 7-day rule, material participation tests, and current state-level scrutiny

The stakes keep rising. The U.S. short-term rental market is projected to hit $76.46 billion in 2026 and grow to $125.14 billion by 2033 at a 7.3% CAGR.[1] AirDNA tracked 2.4 million U.S. STRs generating $64 billion in annual revenue as of 2023.[2] With more revenue flowing through the sector, regulators, owners, and the IRS are all paying closer attention to how operators keep their books.

Why Short Rental Business Accounting Is Different (and Why It Matters Now)

STRs don't behave like long-term rentals or hotels. A single booking can include base nightly rent, a cleaning fee, a pet fee, damage protection, and an early check-in upcharge — all in one transaction. Guests pay months before they arrive. Owners expect a clean monthly statement. The IRS may or may not consider the activity a rental at all, depending on average stay length and services provided.[4]

Add platform payouts, occupancy taxes, and trust-fund obligations, and a generic Schedule E mindset falls apart fast. If you've been managing the back office with a spreadsheet and good intentions, the operational complexity catches up quickly past a handful of units. The rest of this article walks through what to do instead — and Optimal's team supports operators who need specialized bookkeeping for real estate and STR portfolios at every stage.

1. Build a Chart of Accounts That Matches How STRs Actually Earn Revenue

STR revenue is rarely a single line item. A typical three-bedroom Florida vacation home stay can include a $300/night base rate, $200 cleaning fee, $50 pet fee, $79 damage protection, and $50 early check-in — totaling $1,179+ per stay.[3]

If all of that lands in a single "rental income" account, you've already lost visibility. Pass-through fees get tangled with operating revenue. Margin per property becomes a guess. And when tax season arrives, you can't cleanly separate lodging income from service income — which matters more than most operators realize.

1.1 Revenue Accounts to Set Up

At minimum, set up dedicated accounts for each revenue stream:

- Base rental income — the nightly rate only

- Cleaning income — typically $150-300 per stay[3]

- Pet fees — $25-100 per pet per night

- Damage protection — $49-99 per stay

- Early check-in / late checkout — $25-75

- Amenity fees — pool heating, beach equipment, hot tub, etc.

- OTA commission income — for managers earning from listings

This level of detail matters because cleaning fees are commonly reimbursable pass-throughs — bundling them with rent inflates gross revenue and distorts taxable income.[3]

1.2 Expense Accounts and Capitalization Lines

On the expense side, separate the categories that owners and the IRS care about:

- Maintenance and repairs

- Supplies and consumables

- Marketing and listing fees

- OTA fees (Airbnb, Vrbo, Booking.com)

- Insurance

- Utilities

- Contractor and cleaning labor[3]

Just as important: preserve asset-level detail in fixed assets. Cost segregation and bonus depreciation become powerful only when you can identify what was placed in service, when, and at what cost. Under P.L. 119-21 (the "One Big Beautiful Bill Act," signed July 4, 2025), 100% bonus depreciation was restored for property acquired after January 19, 2025.[4] If your books lump furniture, appliances, and capital improvements into a single "renovations" line, you can't claim it cleanly.

With the chart of accounts dialed in, the next discipline is keeping the money in those accounts properly segregated.

2. Apply Trust Accounting: Separate Guest, Owner, and Operating Funds

Trust accounting is the discipline of managing three distinct money flows so funds are never commingled.[3] For property managers, it's not optional — many states regulate trust accounts under real estate licensing law, and commingling can trigger penalties on top of bookkeeping errors.

2.1 The Three Money Flows

| Fund Type | What It Hold | Why It's Separate |

|---|---|---|

| Guest funds | Security deposits, advance booking deposits (often 6-12 months out), reserve holdings | Belongs to the guest until earned or refunded |

| Owner funds | Net rental income owed to property owners, maintenance escrows | Held in trust for the owner; not your revenue |

| Operating funds | Management commissions, OTA payouts to you, your company's own revenue | The only bucket that is actually yours |

Mixing these is the single fastest way to fail a state audit or lose an owner's trust.[3]

2.2 Handling Deferred Revenue and Booking Deposits

Here's where STR accounting breaks most operators: deposits often arrive 6-12 months before a stay. That money cannot be recorded as immediate income. It must sit on the balance sheet as a liability (deferred revenue) until the guest actually checks in and the service is delivered.[3]

"It's a dichotomy of having both an accrual accounting system and a cash accounting system, and it breaks people's brains."

— Jed Stevens, Koloa Kai Vacation Rentals[3]

Get this wrong and you'll overstate revenue, pay tax on money you haven't earned, and misrepresent owner statements. Operators scaling past a handful of units often bring in virtual bookkeeping support to handle deferred revenue logic correctly inside their property management software and accounting stack.

Trust accounting only works if you reconcile it on a strict cadence — which is where the monthly close comes in.

3. Run a Disciplined Monthly Close and Owner Reporting Cycle

Monthly close should be a recurring system, not a cleanup project. Before they automated, the Host & Home team reportedly spent "2-3 full days on month-end reconciliation" stuffing receipts in envelopes.[3] Multiply that across a year and you've burned a full work-month on cleanup that should have been five hours.

3.1 The Daily Capture Loop

Clean monthly closes start with clean daily inputs. Build a capture loop that includes:

- Real-time receipt capture via mobile app at point of purchase

- Property-level tagging on every transaction

- Automated categorization based on vendor and account rules

- Digital storage so receipts are searchable in minutes, not after a 25-minute hunt for a three-month-old charge[3]

"If you don't know your numbers, you don't know anything about your business."

— Nick Giordano, Elevated Tahoe Properties[3]

3.2 The Month-End Close Checklist

A repeatable close usually follows this order:

- Review all transactions for the period

- Match receipts to specific bookings and properties

- Categorize costs by property and account

- Reconcile each trust account (guest, owner, operating)

- Verify OTA payouts against platform statements

- Produce owner statements and distribute payouts

The step that recovers the most margin is splitting reimbursable costs from owner-billable expenses. This is exactly where that 5-10% leakage hides.[3]

3.3 Owner Statements That Build Trust

An owner statement is your monthly proof of stewardship. It should clearly show:

- Gross bookings for the period

- OTA fees deducted

- Cleaning and other pass-throughs

- Management commission

- Net payout to owner

Each line should tie back to a property-level ledger an owner can audit. When it doesn't, you get the experience this operator described:

"We always had a delay in our maintenance team getting us answers to all the bookkeeping questions. A lot of people were involved and nothing was streamlined."

— Aidan Groll, Blue Gems Management[3]

Clean monthly close protects margin. Clean tax documentation protects the entire business.

[caption id="attachment_229702" align="alignnone" width="1376"] Key Short-Term Rental Accounting Statistics for Property Managers[/caption]

Key Short-Term Rental Accounting Statistics for Property Managers[/caption]

4. Get Tax Classification and Compliance Documentation Right

How you categorize stays, hours, and services determines whether the IRS treats your STR as a passive rental or an active trade or business.[4] The difference can mean tens of thousands in deductions — or self-employment tax you didn't expect.

4.1 The 7-Day and 30-Day Rules

Two IRS thresholds drive the classification:

- The 7-day rule: If the average customer stay is seven days or less, the property may be treated as a trade or business rather than a passive rental activity.[4]

- The 30-day rule: If the average stay is 30 days or less and the taxpayer provides significant personal services, similar trade-or-business treatment may apply.[4]

"Hotel-like" services — daily housekeeping, concierge, meals — can push income toward operating-business treatment and potentially trigger self-employment tax. That's why lodging income and service income should be tracked separately in your chart of accounts from day one.[4]

4.2 Material Participation and Grouping Elections

To unlock active-business loss treatment, the taxpayer typically needs to satisfy one of the seven material participation tests. The most common include:

- More than 500 hours of participation during the year

- Substantially all the participation in the activity

- More than 100 hours with no other person participating more

The catch: hours must be logged contemporaneously.[4] A spreadsheet built the week before an audit doesn't hold up. Build the log into the operating workflow.

For multi-property owners, the grouping election under IRS Reg. §1.469-4 allows STRs to be treated as a single activity if economically reasonable and formally elected on the return.[4] This is often the difference between passing or failing the 500-hour test across a portfolio.

4.3 State and Platform Compliance Trends

State and cross-border scrutiny is intensifying:

- Maryland: The Comptroller is examining short-term rentals statewide to ensure proper tax reporting and collection (Aug 2025).[5]

- Florida: HB 7031 took effect Oct. 1, 2025, changing parts of the commercial real estate tax environment relevant to STR-heavy portfolios.[6]

- Costa Rica: A 12.75% tax on platform-generated rental income is set to be enforced starting at the end of 2026 — relevant for any operator with international properties.[7]

The defensive move is simple: maintain an audit-ready folder per property containing booking records, participation logs, occupancy tax filings, and platform 1099-K reconciliations. Operators who already manage compliance documentation across portfolios tend to centralize these into a single shared drive structure mirrored in the accounting system.

The right systems also depend on how big your portfolio is — what works for four units breaks at forty.

5. Scale Your Short Rental Business Bookkeeping by Portfolio Size

Bookkeeping needs evolve with portfolio size. The controls that protect a solo host are overkill for them — and the controls that protect a 50-unit manager are nowhere near enough.

5.1 Solo Hosts (1-4 Units)

Cash-basis bookkeeping is often acceptable at this scale. Even so, do three things from day one:

- Separate revenue lines (don't bundle cleaning into rent)

- Track participation hours for the 7-day rule[4]

- Reconcile each platform payout monthly

These habits cost almost nothing to start and pay off enormously when you add unit five.

5.2 Growing Managers (5-49 Units)

This is the breaking point for most operators. At this scale, move to:

- Accrual or hybrid accounting to properly handle deferred deposits[3]

- Formal trust accounting with segregated bank accounts

- Property-level tagging on every transaction

- A documented month-end close calendar with owner statement templates

Hiring and retaining reliable back-office staff becomes the bottleneck here. Many operators in this range bring in outsourced bookkeeping precisely because internal hires can't keep pace with portfolio growth.

5.3 Multi-Entity Portfolios (50+ Units)

At this scale, the accounting stack itself becomes operational infrastructure. Implement:

- Entity-level consolidation across LLCs

- Intercompany reconciliation for shared services

- Segregated trust accounts by jurisdiction where required

- After-hours coverage for owner inquiries and emergency maintenance billing

A manager with 50+ listings reportedly spent 25 minutes finding a single three-month-old charge under weak recordkeeping.[3] Across a year, that kind of friction kills margin and burns out staff. This is the scale where outsourced back-office support — for cleanup, ongoing reconciliation, and after-hours coverage — usually pays for itself within a quarter.

Conclusion: Clean Books Protect Profit and Pass Audits

The three pillars come back to this:

- A chart of accounts that mirrors real STR revenue streams — base rent, cleaning, pet fees, damage protection, amenities — so margin and tax classification are visible.

- Trust accounting that keeps guest deposits, owner funds, and operating revenue in separate buckets, with deferred revenue properly recorded.

- Tax-aware documentation aligned with the 7-day rule, material participation tests, the §1.469-4 grouping election, and rising state scrutiny.[3][4][5]

The stakes are concrete: 5-10% of reimbursable expenses are at risk without clean reconciliation, and tax misclassification can cost far more in lost deductions or audit penalties.[3][4]

A practical next step before your next tax cycle:

- Run a software audit to surface miscategorized transactions and missing pass-through splits

- Fix the chart of accounts so revenue streams are separated

- Implement a monthly close calendar with reconciliation checkpoints

- Build a per-property compliance folder with participation logs and tax filings

If you'd rather have that audit done for you — and walk away with a clear cleanup plan, a working monthly close, and a managed bookkeeping system that scales with your portfolio — Optimal's team handles exactly this work for real estate and STR operators. A free strategy call and software audit is a low-friction way to see where the leaks are before they cost you another tax cycle.

FAQs

What bookkeeping system is recommended for short-term rental properties?

For solo hosts with 1-4 units, cash-basis bookkeeping in a tool like QuickBooks Online with property-level class tracking is usually enough. Once you cross five units or take advance deposits 6-12 months out, move to accrual or hybrid accounting and add formal trust accounting, with separated bank accounts for guest, owner, and operating funds.[3] Multi-entity portfolios should add entity-level consolidation and intercompany reconciliation on top.

How do you do bookkeeping for your short-term rental?

Start with a chart of accounts that separates each revenue stream — base rent, cleaning, pet fees, damage protection, amenities — and dedicated expense lines for maintenance, supplies, OTA fees, utilities, and labor.[3] Capture receipts in real time with property tags, reconcile every platform payout monthly, and record advance deposits as deferred revenue (a liability) until the stay actually happens. Close the books each month with a checklist and produce an owner statement showing gross bookings, fees, commission, and net payout.

What is the loophole for vacation rental tax (the 7-day rule)?

The "7-day rule" isn't a loophole so much as an IRS classification threshold: if the average customer stay at a property is seven days or less, the activity may be treated as a trade or business rather than a passive rental.[4] Combined with material participation (commonly 500+ hours, or 100+ hours with no one participating more), this can allow losses to offset active income instead of being trapped as passive. Hours must be logged contemporaneously to hold up under audit.

What are the basic principles of bookkeeping for STR operators?

Three principles do most of the work: (1) separate every revenue stream and expense category in the chart of accounts so margin and tax treatment are visible; (2) never commingle guest, owner, and operating funds — trust accounting is both a legal and operational requirement; and (3) record advance deposits as deferred revenue, not income, until the stay is delivered.[3] Layer a monthly close cycle and per-property compliance folder on top and you have an audit-ready system.

How much should I expect to pay a bookkeeper for a short-term rental business?

Pricing varies by portfolio size, transaction volume, and whether the engagement includes trust accounting, owner statements, and tax-ready documentation. Solo hosts can often get by with a few hundred dollars per month, while growing managers with 10-50 units typically invest more given the complexity of deferred revenue, multi-property tagging, and owner reporting. The right benchmark isn't the lowest hourly rate — it's whether the bookkeeper recovers the 5-10% reimbursable expense leakage and keeps you audit-ready, which usually more than pays the fee.[3]

You might also be interested in

100% Match Guarantee

We stand by the quality of our Team Members and guarantee that you will be 100% satisfied with the Team Member assigned to you. If you don't see the value-add, we'll replace and train a new Team Member for free.