Virtual Bookkeeping for Real Estate: A Smarter Way to Scale Back-Office Operations

June 21, 2026

If you manage a growing real estate portfolio and your bookkeeping still runs on spreadsheets, shoebox receipts, or a QuickBooks file nobody fully understands—you already know something is broken. The fix isn't hiring another admin. It's building a managed financial operations layer that scales with you.

Virtual bookkeeping for real estate is a remote, professionally staffed bookkeeping service designed for the structural complexity of property management, investment, construction, short-term rentals, and hospitality businesses. It's not just software. It's trained people operating that software on your behalf—handling reconciliation, entity-level reporting, compliance deadlines, and monthly closes so you don't have to.

Here's what this guide covers:

- Why real estate bookkeeping is structurally harder than standard small business bookkeeping—multi-entity structures, revenue diversity, and layered compliance

- How the virtual bookkeeping workflow actually operates, from bank feeds to monthly close

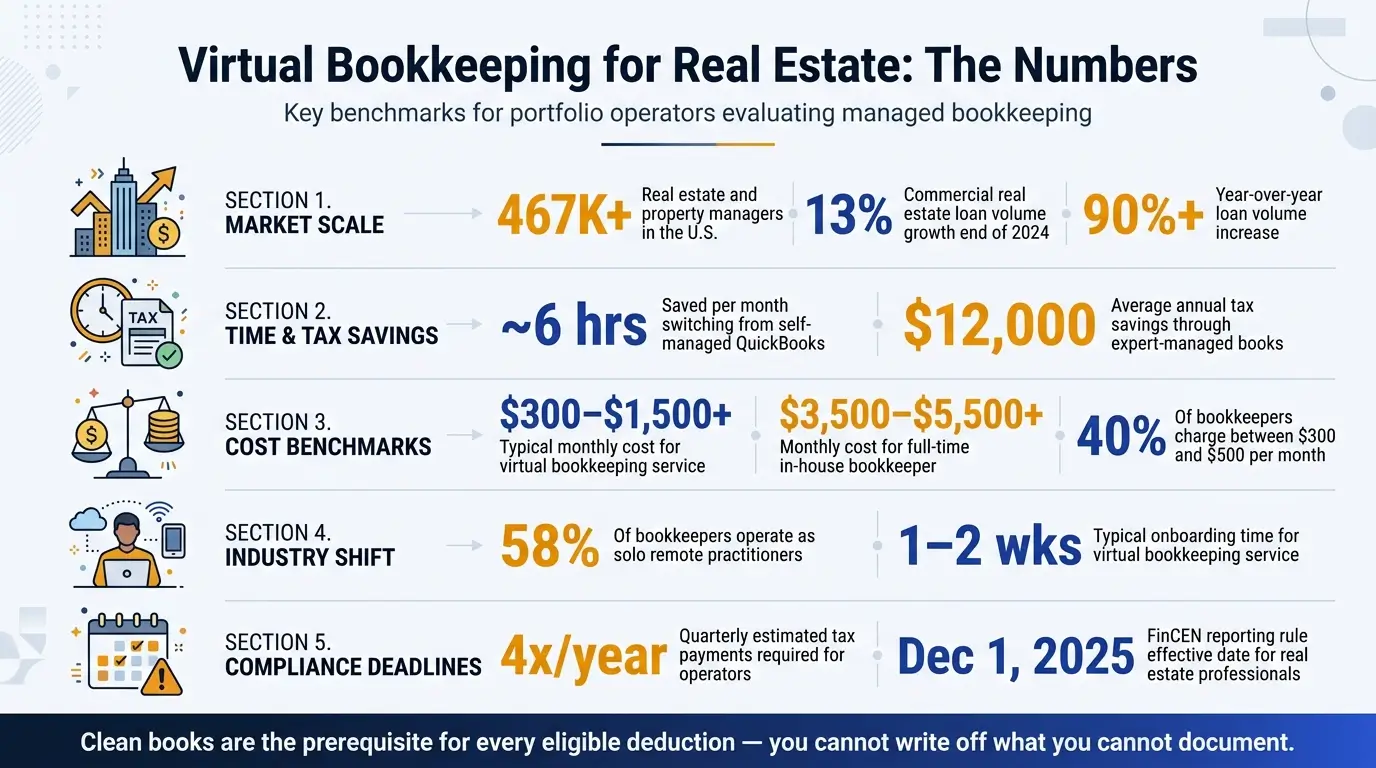

- Concrete ROI benchmarks: operators report saving ~6 hours/month[1] and an average of $12,000/year in tax savings through accurate, expert-managed books[2]

- Cost reality: most services run $300–$1,500+/month versus $3,500–$5,500+ for a full-time in-house hire[9]

- A compliance calendar with monthly, quarterly, and annual checkpoints every operator should follow

- How to evaluate and onboard a virtual bookkeeping provider without losing months to setup

This article is for owners, operators, and executives managing growing portfolios who need reliable financial operations—without building a large in-house team. With over 467,000 real estate and property managers in the U.S.[3] and commercial real estate loan volume up 13% from end of 2024 and over 90% year-over-year[10], the transaction volume hitting back offices right now is not slowing down. Your bookkeeping infrastructure needs to keep pace.

Why Real Estate Bookkeeping Is More Complex Than Standard Small Business Bookkeeping

Most bookkeeping advice on the internet is written for solo agents or single-LLC landlords.[4][5] That advice breaks the moment you're operating across multiple entities, asset classes, or jurisdictions.

Here's what makes real estate bookkeeping structurally different:

Multi-Entity Structures

Real estate operators rarely run a single business. You might have separate LLCs for each property, a holding company, one or more SPVs for syndicated deals, and a management company collecting fees. Each entity needs its own chart of accounts, its own bank reconciliation, and its own financial statements. A generic bookkeeper who's used to handling one set of books for a retail shop will struggle with this from day one.

Revenue Diversity

Your income doesn't come from one source with one recognition pattern. Property management fees, rental income, construction draws, short-term rental nightly rates, and commission income each follow different rules for when and how they hit your books. A single operator might deal with all five of these simultaneously across different entities.

Expense Complexity

CAM reconciliations, maintenance reserves, owner distributions, security deposit tracking, insurance premiums, and vendor payments across dozens of contractors—these create layered expense tracking requirements that go far beyond a simple income-and-expense ledger. Miss one, and your P&L is wrong. Miss several, and your tax return is wrong.

Compliance Layers That Keep Growing

Federal tax obligations are just the start. State-level landlord-tenant accounting rules vary widely. And new regulations keep arriving—for example, the FinCEN reporting rule effective December 1, 2025, applies to certain professionals involved in residential real estate closings and transfers to legal entities or trusts.[3] If your documentation isn't audit-ready, you're exposed.

On top of all this, self-employed operators and pass-through entities must manage quarterly estimated tax payments—due four times per year—which means year-round bookkeeping accuracy isn't optional. It's a requirement.[2]

This level of complexity is exactly why generic tools and DIY approaches start failing as portfolios grow—and why understanding the actual workflow of virtual bookkeeping matters.

How Virtual Bookkeeping for Real Estate Actually Works

A lot of competing articles either list software tools or rank vendors. Few explain how the work actually gets done. If you're evaluating virtual bookkeeping for real estate, you need to understand the operating model—not just the brand names.

The Core Workflow: From Bank Feed to Monthly Close

Here's what a well-run virtual bookkeeping engagement looks like, step by step:

- Connect bank and credit card accounts to the accounting platform (QuickBooks, Xero, or your property management software's built-in accounting module)

- Automate transaction imports so data flows in daily without manual entry

- Categorize transactions by entity, property, and expense type—this is where the real work happens

- Reconcile monthly to ensure every dollar matches between bank statements and your books

- Produce financial statements—profit & loss, balance sheet, and cash flow—for each entity

- Deliver reports on a defined schedule for owner review and decision-making

The critical thing to understand: software handles the repetitive data collection and matching, but trained bookkeepers handle the exceptions, complex categorization, and entity-level accuracy. Bench describes this as a hybrid approach combining automation with dedicated human support.[1]

The glue holding this together is a monthly close discipline—a defined calendar where books are closed by the 10th to 15th of the following month. Without this, you're making decisions based on quarter-old estimates instead of current data.

Document controls matter too. Receipt collection, lease abstracts, 1099 backup, and vendor W-9 management should all be systematized within the virtual workflow. If these are handled ad hoc—"I'll send that receipt later"—the whole system degrades.

What a Virtual Bookkeeping Team Actually Handles

Let's break this into the three tiers of work a competent virtual team covers:

Recurring tasks (monthly):

- Transaction categorization across all accounts and entities

- Bank and credit card reconciliation

- Accounts payable and receivable tracking

- Owner statement preparation

- Tenant ledger support

- Monthly financial reporting packages

Periodic tasks (quarterly/annual):

- Flagging unusual transactions or discrepancies

- Cash-flow alerts when reserves dip below thresholds

- Budget-vs-actual variance reporting

- Coordination with your CPA or tax advisor for filing

This is where virtual bookkeeping diverges sharply from DIY or software-only approaches. Cloud tools like QuickBooks, Xero[6], or Landlord Studio[8] can handle data entry and generate reports. But they don't manage the workflow, enforce deadlines, or catch entity-level errors. That requires trained staff operating them consistently.

Understanding the workflow is one thing. But operators evaluating this shift need to see the numbers—so let's look at the actual business case.

The Business Case: Time Savings, Tax Impact, and Cost Benchmarks

Vague promises about "saving time" and "reducing stress" don't help you make a decision. Here are the actual numbers.

Time and Tax Savings

Time recaptured: A customer testimonial on Bench's realtor page reports saving approximately 6 hours per month after switching from self-managed QuickBooks to a managed bookkeeping service.[1] That's for a relatively straightforward operation. For a portfolio operator managing multiple entities, the cumulative time savings could be two or three times that.

"Bench helped me replace QuickBooks, and save about 6 hours per month of horrible accounting work, which is priceless." — Chris Ronzio, CEO, Trainual[1]

Six hours a month might not sound dramatic. But multiply it across 12 months and factor in the mental overhead of context-switching between bookkeeping and actual operations. That's time you're not spending on acquisitions, tenant relationships, or construction oversight.

Tax optimization ROI: 1-800Accountant reports that its clients save an average of $12,000 per year through expert-driven tax optimization tied to accurate bookkeeping.[2] For real estate operators specifically—where deductions span depreciation, repairs, travel, home-office use, and more—clean books are the prerequisite for capturing every eligible write-off. You can't deduct what you can't document.

Reduced audit risk: Organized, reconciled books with supporting documentation reduce the likelihood of costly errors during IRS audits or lender due diligence reviews. When a lender asks to see your trailing 12-month financials for a refinance, the answer should be "here's the report," not "give me three weeks."

What Virtual Bookkeeping Costs

NerdWallet reports that bookkeeping services typically start at $300 or more per month, with pricing scaling based on transaction volume, entity count, and service complexity.[9]

A 2025 survey of 644 bookkeepers found that 40% charge between $300 and $500 per month, and 58% of those bookkeepers operate as solo practitioners[12]—evidence that virtual delivery is already the dominant model, not some experimental outlier. Broader industry data confirms this trajectory, with cloud adoption and automation accelerating the shift toward remote bookkeeping delivery.[13]

But the real question isn't "what does it cost?" It's "what does it cost compared to the alternative?"

| Factor | In-House Bookkeeper | Virtual Bookkeeping Service |

|---|---|---|

| Monthly cost range | $3,500–$5,500+ (salary + benefits) | $300–$1,500+ (varies by scope) |

| Onboarding time | 2–6 weeks (hiring + training) | Typically 1–2 weeks |

| Software management | Operator's responsibility | Usually included or managed |

| Scalability | Requires additional hires | Scales with portfolio growth |

| Industry expertise | Depends on individual hire | Often built into the service team |

| Coverage gaps (PTO, turnover) | Direct risk to operator | Managed by the service provider |

A single-entity rental portfolio will naturally cost less than a multi-entity operation with STR, construction, and property management arms. Expect to pay more for complexity, not just transaction volume. Providers like Optimal structure pricing around the actual scope of work—entities managed, transaction volume, reporting needs—rather than a flat rate that under-serves complex portfolios.

The numbers make the case. But saving money and time only matters if you're also staying compliant—which brings us to the calendar every operator should be following.

Compliance Checkpoints Every Real Estate Operator Should Build Into Their Bookkeeping Calendar

Compliance is mentioned in nearly every article about real estate bookkeeping. But almost none of them give you a structured, calendar-driven system. Here's what that actually looks like.

Monthly Checkpoints

- Bank and credit card reconciliation for every entity

- Owner statement preparation and distribution

- Expense categorization review (catch miscodings before they compound)

- Security deposit ledger updates (required by law in most states to maintain in separate accounts)

Quarterly Checkpoints

- Estimated tax calculation and payment—due dates: April 15, June 15, September 15, January 15[2]

- Budget-vs-actual review across entities and properties

- Cash reserve assessment (do your maintenance reserves match projected needs?)

Annual Checkpoints

- 1099 preparation and distribution (January deadline—miss it and you're facing penalties)

- Year-end close and tax-package assembly for your CPA

- W-9 collection from all new vendors engaged during the year

- Depreciation schedule updates for all properties

Regulatory Monitoring

- Track new obligations like the FinCEN reporting rule for real estate professionals involved in certain residential closings, effective December 1, 2025.[3]

- Ensure closing-related documentation and entity transfer records are audit-ready

- Stay current on state-level landlord-tenant accounting changes

Here's the reality: the most common failure mode for operators managing books themselves is not getting the math wrong—it's missing deadlines. A quarterly payment slips. A 1099 goes out late. A reconciliation gets pushed to "next week" for three months straight.

A dedicated virtual bookkeeping team with playbooks and recurring task calendars prevents this. The cadence is built into their workflow, not dependent on your memory.

Knowing what to track is one thing. Knowing how to pick the right team to track it is another—let's cover that next.

How to Evaluate and Onboard a Virtual Bookkeeping Service for Real Estate

Not all virtual bookkeeping services are built for real estate. Many are generalist operations that handle e-commerce stores, restaurants, and freelancers—then try to bolt on property management clients as an afterthought. Here's how to separate the two.

Key Evaluation Criteria

Industry-specific experience. This is the single most important filter. Does the provider understand property management trust accounting? STR revenue recognition? Construction draw schedules? Multi-entity consolidation? Generic bookkeeping firms often lack this depth entirely.[11]

Software proficiency. Confirm the provider works with your existing tools—QuickBooks, Xero, AppFolio, Buildium, Gusto, or whatever your stack includes.[6][7] Equally important: can they handle cleanup or migration if your current books are messy? Software cleanup and migration is one of the most common pain points operators face when switching services—ask directly how the provider handles it.

Security and data controls. Virtual bookkeeping means granting access to bank accounts, credit cards, and financial platforms. Ask about:

- Access policies (who can see what, and how access is revoked when team members change)

- Encryption and data handling protocols

- Team vetting and background checks

- Whether they use read-only access where possible

Dedicated vs. pooled staffing. Some services assign you a dedicated bookkeeper or team. Others use a rotation model where whoever's available picks up your tasks. For complex real estate portfolios, dedicated teams build deeper context over time—they learn your entities, your vendors, your quirks. That matters.

Scalability. Your provider should grow with you. Adding a new entity, onboarding a short-term rental arm, or expanding into construction shouldn't require a full re-engagement process. Ask: "What happens when I add three more LLCs next quarter?"

What to Expect During Onboarding

A well-structured onboarding typically follows this sequence:

- Initial strategy call and software audit—the provider reviews your current tools, entity structure, and pain points

- Assessment of cleanup needs and timeline—how far behind are your books? What needs to be fixed before ongoing work can start?

- Account access setup and document collection—bank connections, software credentials, prior-year returns, lease files

- Historical cleanup (if needed)—reconciling past months or years to establish a clean starting point

- Transition to recurring monthly bookkeeping—with defined deliverables, close dates, and communication cadence

A cleanup phase is normal. Operators switching from DIY or poorly maintained books should expect this to take 2–8 weeks depending on the backlog. Don't be alarmed by this—it's a necessary foundation. Skipping cleanup means building accurate ongoing books on top of inaccurate historical data, which defeats the purpose.

Set expectations upfront: what reports will you receive, and when? What's the close deadline each month? How do you communicate—email, Slack, a shared portal? What's the escalation path if something looks wrong? The best engagements are relationship-based and ongoing, not transactional.[12]

Key Takeaways for Scaling Real Estate Back-Office Operations

Virtual bookkeeping for real estate isn't about outsourcing data entry. It's about building a managed, scalable financial operations layer that supports compliance, tax readiness, and portfolio growth—without requiring you to hire, train, and manage an in-house accounting department.

The market already reflects this shift. With 58% of bookkeepers working solo and remotely[12], virtual delivery is the dominant model. Pricing at $300–$500/month for standard engagements[9] makes it accessible for most operators, with higher-complexity portfolios paying more for the depth they need.

The four outputs that matter most from a strong virtual bookkeeping system:

- A disciplined monthly close—current financials, not quarter-old guesses

- Quarterly tax readiness—estimated payments calculated and filed on time

- Audit-ready documentation—every transaction reconciled, every vendor W-9 collected

- Financial reports that actually inform decisions—not just compliance artifacts

Start by auditing your current bookkeeping gaps. Where is your software falling short? Are you consistently closing books on time? Do you have a compliance calendar, or are deadlines managed by memory? If the answers concern you, it's worth evaluating whether a managed virtual service closes those gaps more reliably than your current approach.

Optimal offers a free strategy call and software audit specifically designed for real estate operators dealing with multi-entity complexity, software cleanup needs, and compliance gaps. If your back office is holding back your growth, that's a reasonable place to start the conversation.

FAQs

How much does virtual bookkeeping for real estate cost?

Most virtual bookkeeping services start at $300 or more per month for straightforward engagements, with 40% of providers charging between $300 and $500 monthly.[9][12] For multi-entity real estate portfolios with STR, construction, or property management complexity, expect pricing in the $800–$1,500+ range. This is still significantly less than a full-time in-house bookkeeper, which typically runs $3,500–$5,500+ per month when you factor in salary, benefits, and management overhead.

What bookkeeping software works best for property managers and real estate investors?

QuickBooks Online and Xero are the most widely used general accounting platforms for real estate, with Xero offering strong cloud-based mobility features.[6] Property-specific tools like AppFolio and Buildium handle tenant ledgers and owner statements natively, while Landlord Studio serves smaller landlord portfolios.[8] The best choice depends on your entity structure and portfolio size—your virtual bookkeeping provider should be proficient in whichever platform fits your operation.

How does virtual bookkeeping help with real estate tax compliance and estimated quarterly payments?

Virtual bookkeeping keeps your books current month-to-month, which means quarterly estimated tax calculations are based on actual income and expenses—not guesses. Quarterly payments are due April 15, June 15, September 15, and January 15, and missing them triggers penalties.[2] A managed virtual team builds these deadlines into their recurring task calendar so nothing slips. They also prepare year-end tax packages and coordinate with your CPA, ensuring deductions like depreciation, repairs, and travel are fully documented and captured.

Is virtual bookkeeping secure enough for multi-entity real estate businesses?

Yes, when you choose a provider with proper security protocols. Look for encrypted data transmission, role-based access controls, team background checks, and the use of read-only bank connections where possible. Reputable providers also have clear procedures for revoking access when team members change. The key is evaluating security practices during your selection process—not assuming they're in place.

When should a real estate operator switch from in-house bookkeeping to a virtual bookkeeping service?

The clearest signals are: your books are consistently behind, reconciliations are months late, you're missing quarterly tax deadlines, or you're spending significant time managing your bookkeeper instead of your portfolio. If you're adding entities or properties faster than your current staff can keep up, or if turnover in your back-office role keeps disrupting your financial operations, a virtual service provides continuity and scalability that a single hire cannot. Most operators find the transition pays for itself within the first quarter through time savings and improved tax accuracy.

You might also be interested in

100% Match Guarantee

We stand by the quality of our Team Members and guarantee that you will be 100% satisfied with the Team Member assigned to you. If you don't see the value-add, we'll replace and train a new Team Member for free.